The market grew by 11.9% year on year, achieving double-digit growth.

This strong performance was driven by a combination of price revisions resulting from rising raw material and logistics costs, together with pet owners’ increasing focus on health and premium-quality products.

In this article, we analyze the outlook for the Japanese pet food industry, examining recent market developments and providing a forward-looking forecast.

The analysis covers the current situation over the past two years as well as projections for the next decade, incorporating key statistical data, market trends, and competitive dynamics among major players.

Market Size and Growth Overview

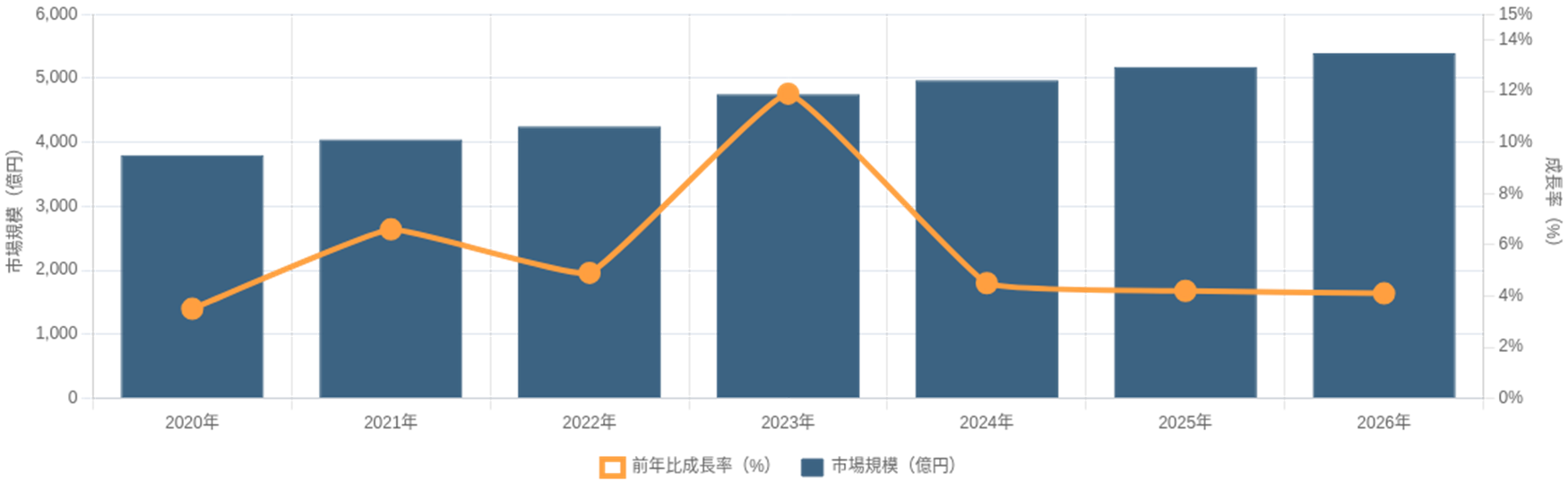

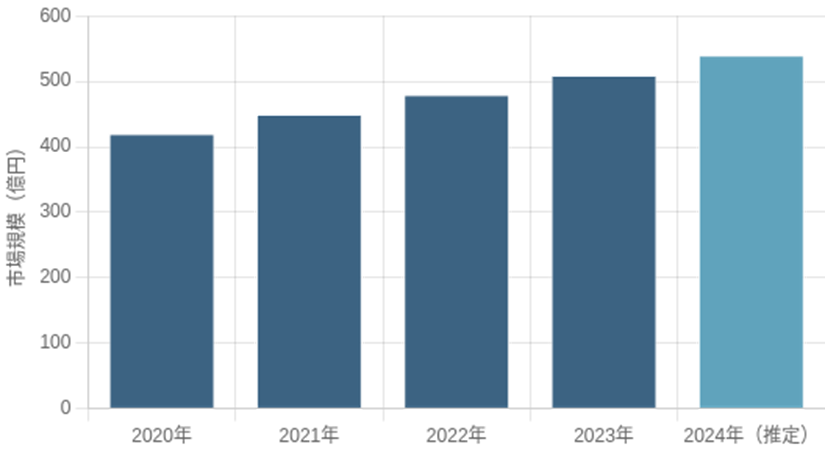

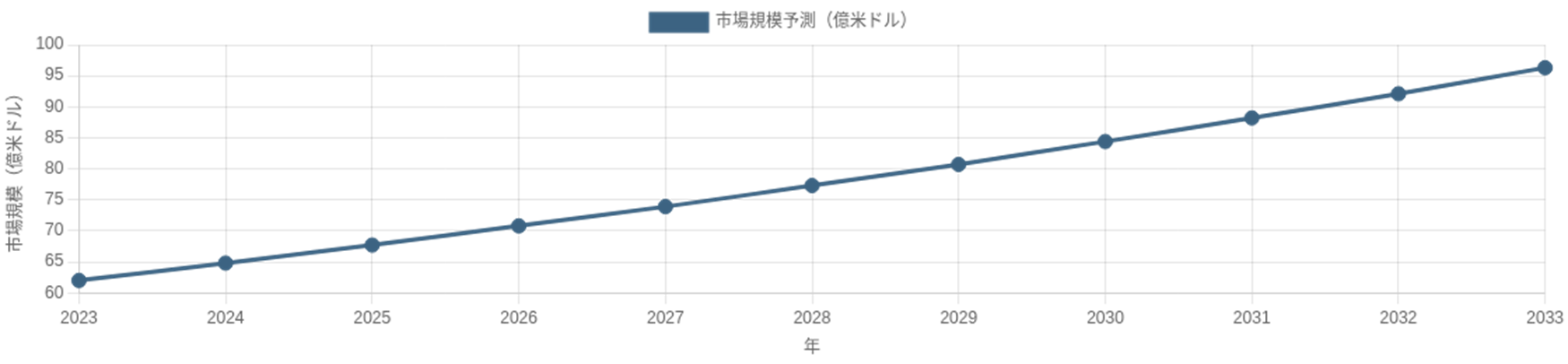

Japanese Pet Food Market: Historical Trends and Forecasts

Despite stagnation in the number of pets, Japan’s pet food market continues to grow. The shift toward higher value-added products and rising health consciousness among pet owners are driving steady market expansion. In particular, 2023 saw double-digit growth, largely influenced by price increases stemming from higher raw material and logistics costs.

Total market size (2023):

¥475.4 billion

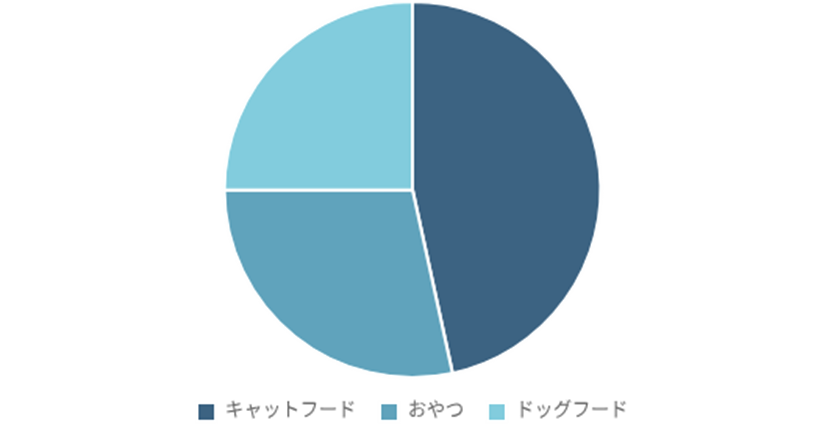

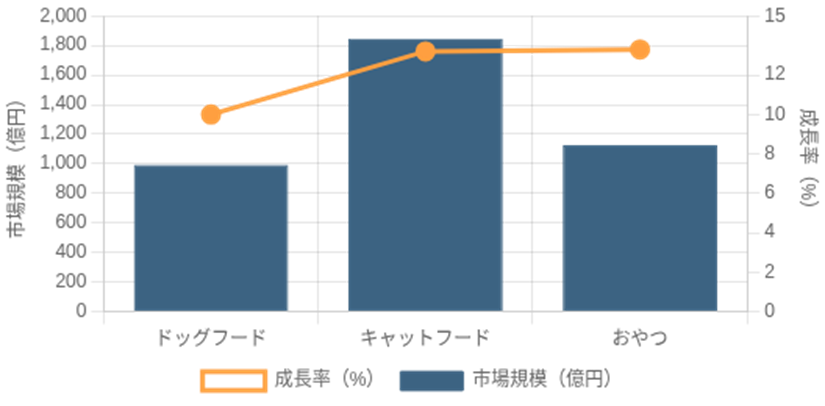

All major categories recorded double-digit growth.

Dog Food

¥99.3 billion

+10.0% year on year

Dry food has returned to a growth trajectory, supported by strong demand for high-protein and additive-free products.

Cat Food

¥184.7 billion

+13.2% year on year

The largest category, yet still posting robust growth. Health-care-oriented products performed particularly well.

Dog & Cat Treats

¥112.5 billion

+13.3% year on year

Functional treats and dental care products drove the highest growth rate among all segments.

In total, the domestic market reached approximately ¥475.4 billion in 2023 (+11.9% YoY). Major categories all achieved double-digit growth: dog food (~¥99.3 billion), cat food (~¥184.7 billion), and dog and cat treats (~¥112.5 billion).

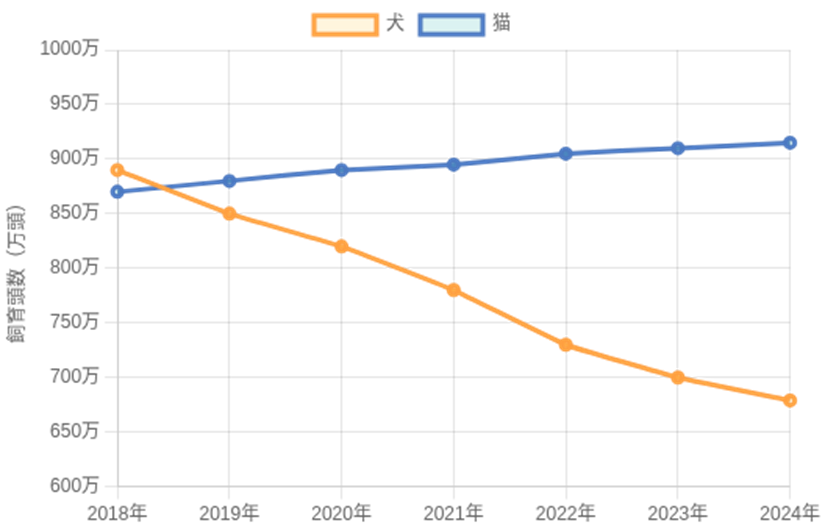

Trends in Dog and Cat Ownership (2018–2024)

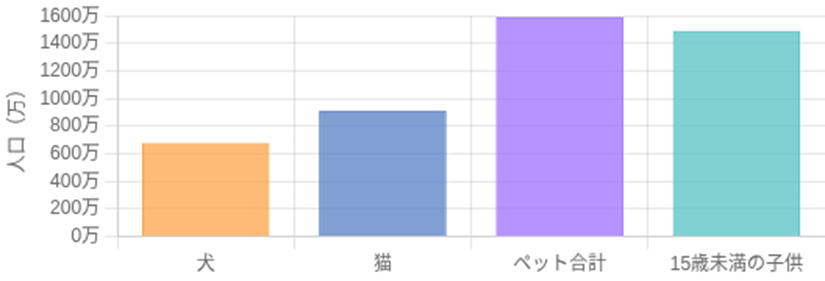

Comparison of the Pet Population and the Child Population in 2024

Against the backdrop of Japan’s declining birthrate and aging population, the number of pets now exceeds the number of children under the age of 15.

As of 2024, the dog population stood at approximately 6.79 million, while the cat population reached 9.15 million, for a combined total of 15.95 million pets, surpassing the population of children under 15 years old.

While the number of dogs is on a gradual decline, the cat population has remained stable. Urbanization, an increase in single-person households, and lifestyle factors are contributing to a growing preference for cats in metropolitan areas.

Although the total number of pets is not increasing significantly, higher spending per pet and greater penetration of premium-priced products continue to push the market upward. As a result, steady market expansion is expected to continue beyond 2024.

According to research firm IMARC, Japan’s pet food market was valued at USD 6.2 billion (approx. ¥680 billion) in 2024 and is forecast to grow at a CAGR of 4.5%, reaching USD 9.6 billion by 2033.

While the strong tailwind from inflation-driven price increases is unlikely to persist, continued demand for premium products and the introduction of new value-added offerings are expected to support moderate growth in value terms. Industry forecasts also suggest that by 2026, the market will expand by approximately 7–8% compared with 2023, indicating ample mid- to long-term growth potential.

- Price revisions due to rising raw material and logistics costs

- Increasing premiumization of pet food

- Growing health awareness among pet owners

- Higher spending per pet

Major Trends in the Pet Food Market

- Premium and Functional Foods:

Demand for premium foods with high nutritional value and functional products addressing specific health needs continues to expand. The therapeutic diet segment alone has exceeded ¥50 billion and is still growing. - Natural and Sustainable Products:

Products emphasizing organic ingredients, grain-free formulations, additive-free recipes, and environmentally conscious manufacturing are gaining traction. Interest in sustainable sourcing is also rising. - Palatability and Gourmet Orientation:

High-quality gourmet foods using human-grade ingredients and marketed as “meals rather than feed” are increasingly popular, particularly fresh and refrigerated/frozen pet foods. - Treats and Supplements:

Functional treats such as dental care snacks, as well as supplements for joint support, gut health, and skin and coat condition, continue to grow at over 20% annually. - E-commerce and Subscription Models:

Online sales channels and subscription services tailored to individual pets’ needs are becoming mainstream, with D2C models gaining prominence.

Expansion of Premium and Functional Foods

Expansion of the Veterinary Channel Therapeutic Diet Market

Growing Demand for Premium Pet Food

High Quality and High Functionality

- Rising popularity of high-protein, high-quality, and high-meat-content diets

- Increasing segmentation of age-specific nutritional formulations

Health and Safety-Oriented Products

- Safety-focused foods made with additive-free formulations and domestically sourced ingredients

- Expansion of allergen-conscious diets that exclude specific ingredients

Therapeutic and Functional Diets

- Products designed to address specific health needs, such as lower urinary tract health and kidney support

- Hill’s launched a new veterinarian-exclusive pet food brand—its first new brand in 20 years—highlighting the growing importance of this segment

As pet owners’ health awareness rises, demand for premium and functional foods continues to grow. In the dog food segment, high-protein, high-meat-content diets and additive-free products have driven renewed growth in the dry food category. In the cat food segment, diets targeting urinary tract and kidney health have become increasingly common.

The aging of pets and their treatment as family members have also boosted demand for senior-specific products addressing joint health, weight management, and digestive support.

The veterinary channel is expanding rapidly, and while foreign brands have traditionally dominated this segment, domestic manufacturers are increasingly entering the market. For example, Hills launched a new veterinarian-exclusive brand in 2024—the company’s first in 20 years—further intensifying competition in the functional premium segment.

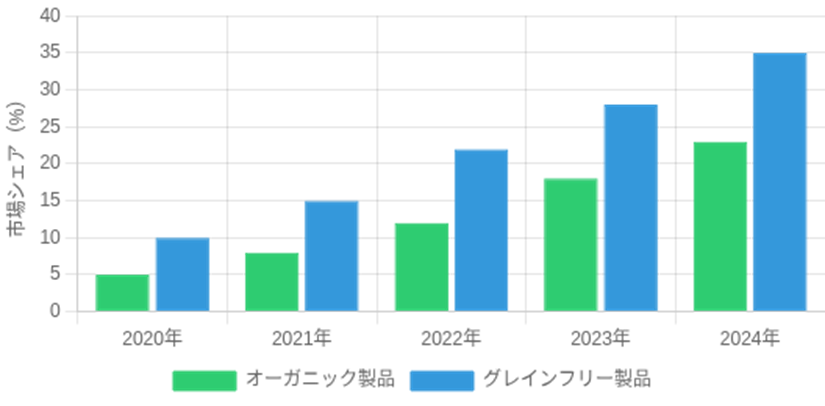

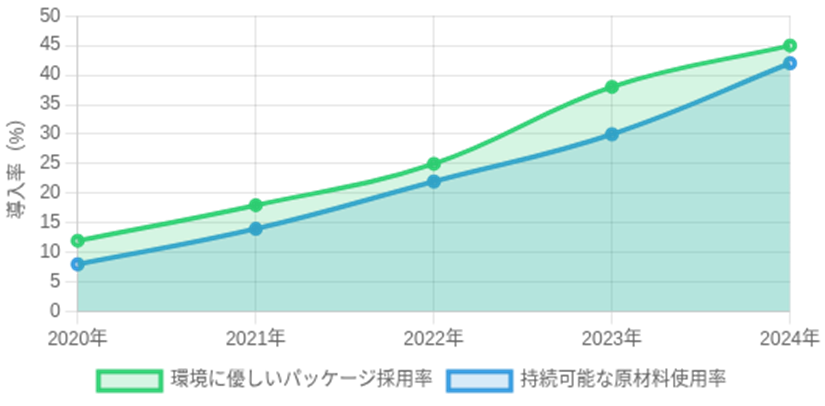

Natural Orientation and Sustainability

Market Share Trends of Natural-Oriented Pet Food Products

Adoption Rate of Environmentally Friendly Pet Food

Organic and Natural Ingredients

- Reflecting growing safety consciousness among pet owners

- Strong preference for organic and naturally sourced ingredients

- Use of ingredients comparable in quality to those used in human food

Grain-Free and Limited-Ingredient Formulations

- Rapidly increasing popularity of grain-free pet food

- Expansion of allergy-friendly and additive-free products

- Greater emphasis on ingredient traceability

Sustainability Initiatives

- Adoption of insect-based protein sources

- Use of biodegradable and recyclable packaging materials

- Reuse of food by-products and efforts to reduce food waste

Growing safety and environmental awareness among pet owners has accelerated demand for organic, natural, grain-free, and additive-free products. There is also increasing scrutiny of the environmental impact of pet food, leading to interest in insect-based proteins, plant-based formulations, and eco-friendly packaging.

Some studies suggest that up to 90% of a pet’s climate impact comes from its diet, highlighting the importance of sustainable materials. In Japan, initiatives such as utilizing food waste ingredients and adopting biodegradable packaging are becoming more common, making sustainability a key factor shaping the future market.

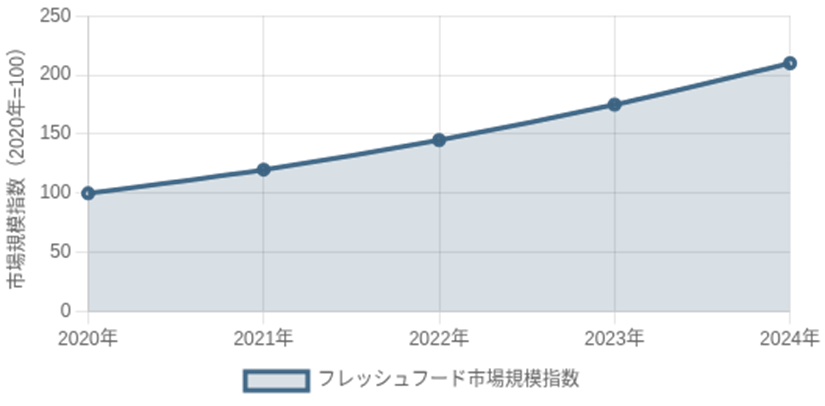

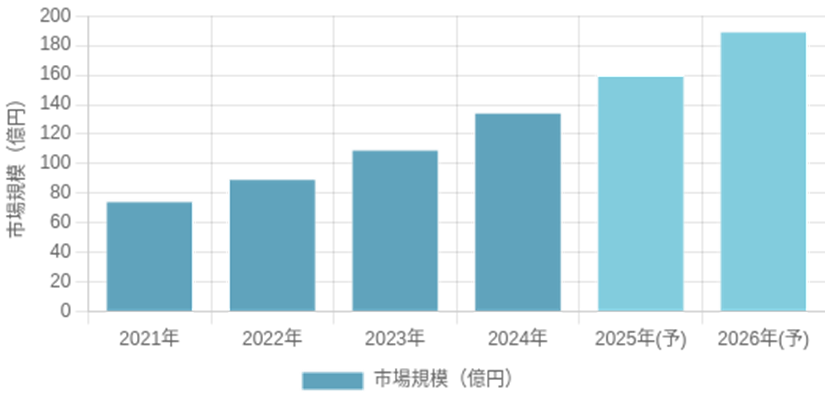

Gourmet Foods, Treats, and Supplements

Growth Rate of the Fresh Pet Food Market

Pet Supplement Market Size and Forecast

“Not Feed, but Real Meals”

- As pets are increasingly regarded as members of the family, demand is rising for foods that are not only nutritious but also tasty and visually appealing—meals that feel more like a “treat” or “home-cooked dish” rather than conventional pet feed.

- Frozen home-delivered pet food services, which offer fresh, hand-prepared meals supervised by veterinarians, have gained widespread adoption and are now used by more than 300,000 dogs and cats combined.

Human-Grade Ingredients

- Pet foods made with **human-grade ingredients—of a quality fit for human consumption—**are attracting growing attention.

- In the super-premium segment, key selling points include the use of domestically sourced, fresh, additive-free, and high-quality ingredients. Products such as frozen meals that can be warmed in a microwave before feeding are designed to closely resemble human meals in both quality and appearance, further reinforcing the “food, not feed” concept.

Treats and Supplements Market

- The treats category is evolving from simple snacks into functional products, such as dental chews and oral-care treats that support daily health maintenance.

- At the same time, the pet supplement market continues to expand at an annual growth rate exceeding 20%. Popular formulations include glucosamine for joint support, probiotics for gut health, and omega-3 fatty acids for skin and coat care, reflecting growing demand for products that actively support pets’ long-term health and quality of life.

Growth of Fresh Pet Food

Fresh pet food delivered refrigerated or frozen is growing at over 20% annually, despite its relatively small market size.

Expansion of the Supplement Market

Rising health awareness has also driven growth in pet supplements, including products for joint health, gut microbiota balance, and skin and coat care.

As pets are increasingly regarded as family members, owners are seeking foods that are not only nutritious but also visually appealing and enjoyable. Gourmet products made with human-grade ingredients and fresh food delivery services exemplify this trend.

For example, domestic startup CoCo Gourmet offers veterinarian-supervised fresh meals delivered frozen and now serves over 300,000 dogs and cats. Such premium offerings are expected to maintain steady demand as companion animal humanization continues.

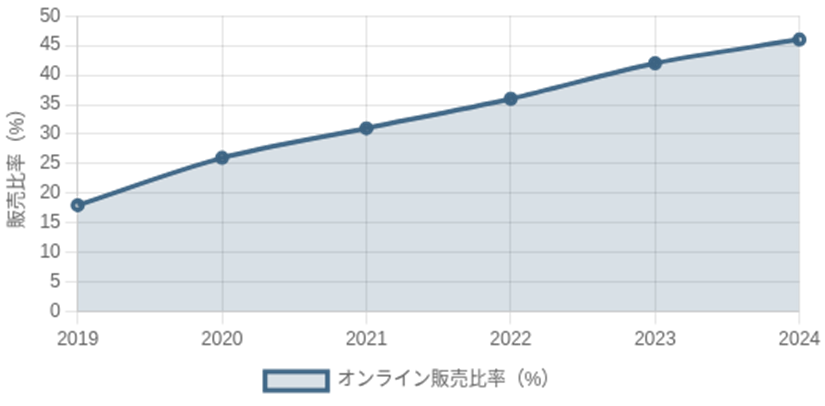

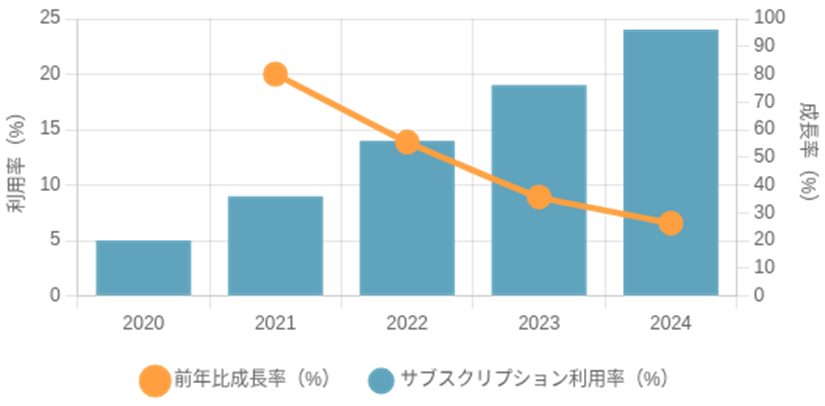

E-commerce and Subscription Model Adoption

Trends in the Online Sales Share of the Pet Food Industry

Subscription (Auto-Replenishment) Service Adoption Rate

Sustained Growth of Subscription-Based Business Models

Improved Convenience

Pet food can be ordered 24/7 and delivered directly to the home, eliminating the need to carry heavy bags from stores. This offers significant benefits for elderly pet owners and those living in rural areas, while also saving time for busy owners.

Expanded Product Selection

Online channels provide access to premium products and niche brands that are often difficult to find in local retail stores. A wide range of offerings is now available, including personalized meal plans and veterinarian-formulated specialty diets.

Transformation of the Customer Experience

Digital platforms enable the proposal of optimal food plans tailored to a pet’s age, breed, and preferences. Personalized recommendations based on web-based assessments, combined with the convenience of subscription delivery, help drive repeat purchases and long-term customer retention.

Online purchasing of pet food continues to expand, providing access to premium and niche brands previously unavailable through local retailers. Subscription models offer convenience, personalized nutrition plans, and consistent delivery, improving customer retention.

These digital channels benefit busy pet owners, elderly consumers, and those in rural areas, while enabling manufacturers to connect directly with customers via D2C strategies, exclusive online products, and targeted promotions.

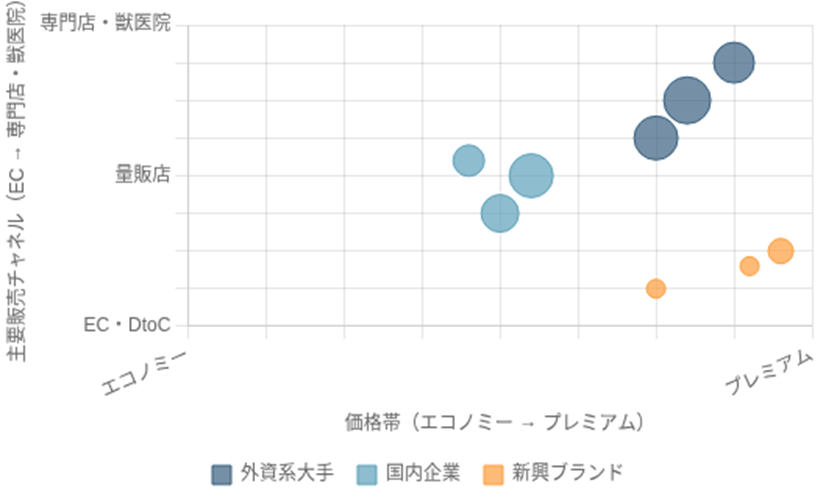

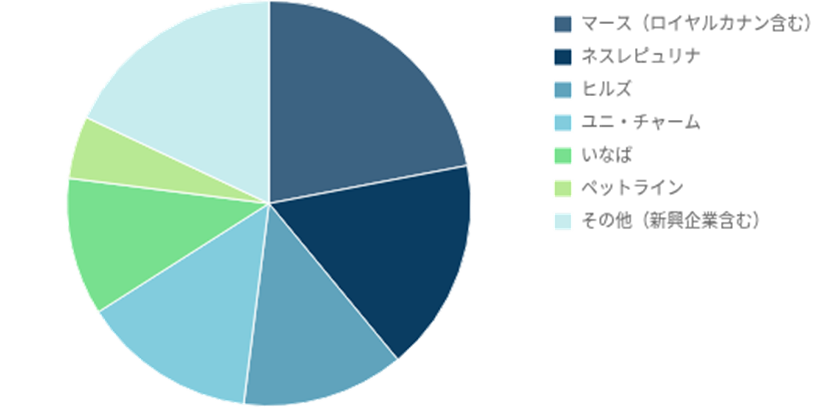

Competitive Landscape and Brand Strategies

Corporate Positioning Map

Estimated Market Share of the Japanese Pet Food Market

Major Global Players

- Mars (Pedigree, Royal Canin)

- Nestlé Purina

- Hill’s (Colgate-Palmolive)

Leading Domestic Companies

- Unicharm (e.g., Gin no Spoon)

- Inaba Petfood (CIAO Churu)

- Petline (domestic comprehensive pet food manufacturer)

Emerging Brands

- Biofilia (CoCo Gourmet)

- PETOKOTO (customized diets)

- Inuneko Seikatsu (additive-free D2C brand)

Multinational Market Leaders

Japan’s pet food market is highly competitive, with major multinational manufacturers, established domestic players, and emerging brands all competing for share. Key global players include Mars (e.g., Pedigree, Royal Canin), Nestlé Japan (Nestlé Purina), and Hill’s (a Colgate-Palmolive subsidiary).

These multinational leaders have held a large portion of the market for many years, with particular strength in complete and balanced nutrition products as well as veterinary therapeutic diets.

Major Domestic Players

Domestic companies also maintain a strong presence. Examples include Unicharm (known for high-quality cat food lines such as Gin no Spoon), Inaba Petfood (widely recognized for cat treats like CIAO Churu), and Petline (a domestic full-line pet food manufacturer), all of which produce and sell dog and cat food products.

In particular, Inaba has an overwhelmingly strong position in the cat wet food and treats category, while Unicharm leverages strong brand power across a broad range of pet-related products—from pet care goods such as diapers to pet food.

These established companies have also been actively upgrading their product portfolios in line with recent trends—for example, launching new lines positioned around zero additives and Japanese-sourced ingredients, and shifting from large-format packages to smaller portioned packs to maintain freshness and reduce food waste. Overall, they continue to respond proactively to evolving consumer preferences.

The Rise of Emerging Brands

The growth of emerging brands and startups is also a notable development. Venture companies have entered the market with distinct approaches, including Biofilia, which operates the fresh pet food delivery service CoCo Gourmet; PETOKOTO, which offers made-to-order pet food; and Inuneko Seikatsu, which sells additive-free products through a D2C model.

These newer players reach younger consumers through digital marketing, leveraging social media and owned media channels. They differentiate themselves through premium positioning and sustainability initiatives—for example, PETOKOTO emphasizes the use of upcycled food materials and environmentally conscious packaging.

Subscription models, in particular, are widely adopted by startups because of their high retention rates and attractive profitability. In response, established major players are also accelerating efforts such as partnering with these newcomers, strengthening their own e-commerce channels, and launching premium sub-brands. As a result, competition is intensifying across the market—while at the same time creating a positive cycle in which new value propositions continue to emerge.

10-Year Outlook and Key Challenges

Market Forecast

High-Growth Segments

- Senior pet nutrition

- Preventive healthcare foods

- Sustainable premium products

- Personalized nutrition services

Key Challenges

- Declining pet ownership, particularly among dogs

- Consumer price sensitivity amid inflation

- Rising costs associated with sustainability initiatives

- Intensifying competition and the need for differentiation

Over the next decade, Japan’s pet food industry is expected to achieve sustained growth and further sophistication. The overall market is likely to expand gradually, with the premium segment in particular acting as a key driver. As Japan’s population continues to age—and as both senior pet owners and senior pets increase in number—the development of nutrition-focused care products tailored to these needs will become even more important.

For example, life-stage-specific products such as low-calorie senior dog food designed to support joint health, or senior cat food formulated to reduce the burden on the kidneys, are expected to become increasingly segmented and advanced.

In addition, pet-related spending is seeing a rising share of medical costs. This trend is likely to accelerate demand for preventive health-oriented foods (e.g., dental care, weight management) and for new service-integrated business models—such as personalized diet recommendations linked to pet insurance.

At the same time, several structural challenges could limit market expansion. The first is the demographic constraint of declining pet ownership. Unless the industry can better address “latent potential owners” who want to keep pets but cannot—through measures such as increasing pet-friendly housing and improving access to pet-sitting and pet-hotel services—the market’s underlying base may weaken over time.

Growing consumer price sensitivity is another concern. As inflation persists, some consumers have begun shifting from higher-priced products to more affordable options, which means companies will need to ensure pricing is clearly justified by added value while also strengthening retention strategies to build repeat purchases. Sustainability is also becoming unavoidable.

Companies that move early to adopt environmentally friendly manufacturing and responsible sourcing are likely to strengthen brand preference and trust, while those that fall behind may face increasing competitive disadvantage—potentially to the point of being pushed out of the market.

Practical Insights for Product Development Leaders

Strengthening Cat Treat Offerings

This is the fastest-growing segment in the market. Development should focus on purée-style and soup-style treats that combine strong communication value with functional benefits, such as kidney health support and hairball control.

Premium and Functional Dry Food

There is strong demand for differentiated products backed by scientific rationale, including high-protein, low-carbohydrate formulations, grain-free recipes, and products containing probiotics to support gut health.

Formulas for Senior Dogs and Small Breeds

While ownership of medium-sized dogs is declining, the proportion of senior dogs continues to increase. This creates opportunities for specialized products featuring softer textures, digestive support, and joint-care ingredients, particularly for senior and small-breed dogs.

Sustainable Ingredients and Packaging

Key initiatives include the use of insect-based proteins, upcycled food by-products, and the adoption of paper-based or bio-plastic packaging. Clearly communicating reduced environmental impact will be critical for differentiation.

Development of Digital Sales Strategies

Manufacturers must adapt to the expansion of e-commerce and subscription-based models. Opportunities include online-exclusive products and personalized nutrition and meal-planning services tailored to individual pets.

Contact Us

Our Overseas OEM Pet Food Support service assists clients with product planning, development, manufacturing, and logistics by connecting them with OEM factories in Thailand, Australia, New Zealand, and Canada.

Supported Product Categories

- Dry dog food

- Freeze-dried raw dog food

- Dry cat food

- Freeze-dried raw cat food

- Dog treats

- Cat treats

- Air-dried pet food

- Retort products

We provide comprehensive support tailored to your needs.

Email

nagai@first-reach.org

We reply within 1 business day.

Phone

+66 (0)6-1457-4310

Weekdays 8:00〜17:00

Web Form

https://first-reach.org/en/contact/

Available 24/7 via smartphone or PC